If you’re dealing with back pain or neck pain and have to work all day at your desk, then it might be time to switch to a standing desk. Have you ever wondered if your insurance company will pay for a standing desk?

The answer is a solid maybe. Depending on your health insurance provider, there is a chance that you can get a standing desk covered by insurance. It may have to do with whether or not you have any medical condition(s) – more on that below.

The first step you need to take is to call your insurance provider up to see if they will cover it.

Contact Your Health Insurance Provider First

In speaking with Kaiser Permanente, one of the largest health insurance companies in the United States, one of the options you may have is to speak to your primary care physician and have them put in a referral to the referrals / prior authorization team at KP, who will review the request.

Under Internal Revenue Service (IRS) rules, some health care services and products are only eligible for reimbursement from your health savings account (HSA), limited purpose flexible spending account (FSA), and health reimbursement arrangement (HRA) when your doctor or other licensed health care provider certifies that they are medically necessary.

Your health care provider must indicate your (or your qualified dependent’s) specific diagnosed medical condition, the specific treatment needed, the length of treatment, and how this treatment will alleviate your medical condition.

Consider writing down your job requirements and the tasks you often perform at work, and then sharing this information with your doctor. Once he or she looks over the information and compares it to your disability and/or medical conditions, your doctor will write you a letter of medical necessity (aka a prescription) for a standing desk if you need it.

What is a Letter of Medical Necessity (LMN)?

Many of the health insurers in the United States *may* provide you with reimbursement through your FSA.

A letter of medical necessity is a doctor’s note that supports the case for you having a standing desk at work. Your chances of having insurance approve the need for a standing desk increase greatly if you obtain a LMN from your doctor.

A stronger case for your health insurance to cover the cost of a standing desk includes having chronic conditions such as:

- cervicogenic headaches

- back pain

- joint pain

- high blood pressure

- discogenic pain

- neck pain

- bad circulation

Sample Letter of Medical Necessity

Each insurance provider should have their own LMN form on their website so be sure to do a Google search for your insurer's LMN. Here is a sample LMN from HealthEquity:

How Much Will My Insurer Reimburse Me for a Standing Desk?

If you confirm that your insurer does cover the cost of your standing desk, they may set limits on the price of the standing desk that they will reimburse you for. There are affordable standing desk options out there that your insurer may be more willing to reimburse you for if that is the case.

A few years ago it was hard to find standing desk converters (desktop converters that converter your existing desk from a stationary desk to a sit stand desk) for under $250. Now, there are plenty of affordable options that your insurance provider or your employer may be willing to reimburse you for.

What standing desk is good for me?

After confirming that your insurance provider will cover the cost of your standing desk, it’s time to shop for a standing desk! A tool we created, called the DeskFinder, helps you find the perfect standing desk for you.

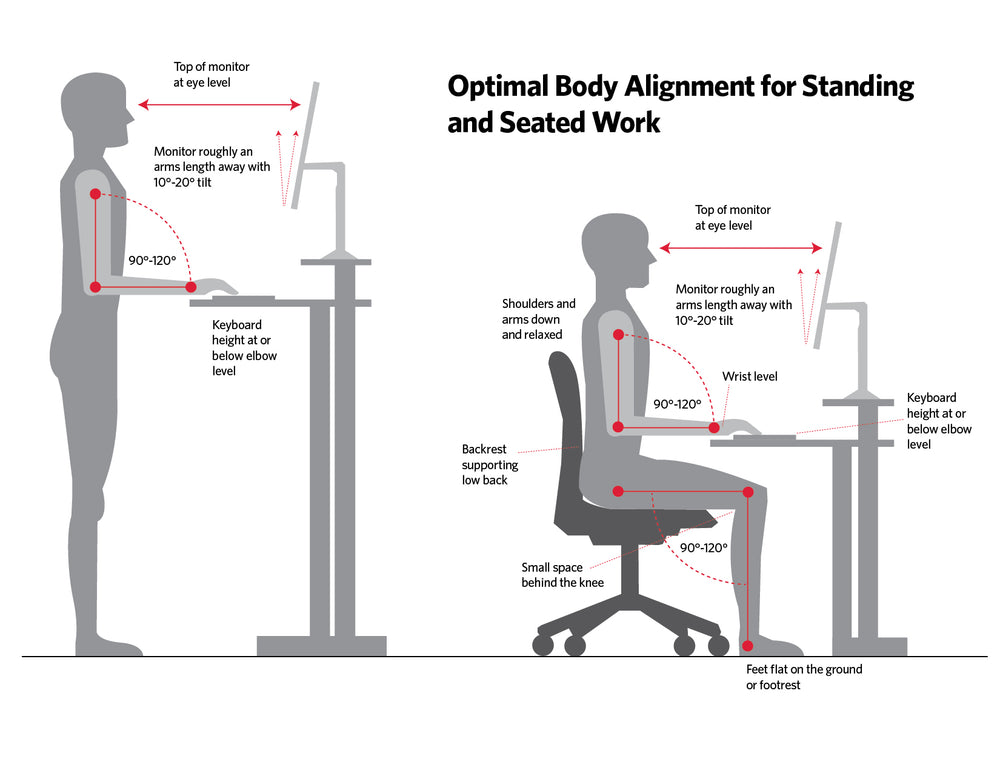

Here are some important standing desk features to keep in mind that might help you out when you’re looking for a desk riser. If you purchase a standing desk, keep your receipt handy for time when you try to get reimbursement.

Some other things to think about regarding getting insurance to cover a standing desk:

- You may need to get an Explanation of Benefits (EOB) from your insurance company. This will show that your purchase was not covered under your insurance.

- You also will need to fill out a claim form. When you signed up for your FSA/HSA you may have received a welcome packet. If not, you could contact your plan administrator or the FSA/HSA provider website to obtain claim forms.

- You will likely have to purchase your ergonomic desk out of pocket and then seek reimbursement.

- If your purchase is covered, you will receive a reimbursement check via the mail or direct deposit into your bank account, depending on how your account was set up. Reimbursement usually will occur within 10-14 days after submission.

What other FSA/HSA eligible products can I purchase?

If you are in need of other eligible products, such as standing desk chairs (or ergonomic chairs), we suggest reaching out to your FSA/HSA administrator to further assist you. To find the contact number for them, check the back of your FSA/HSA card.

What is a Health Savings Account (HSA)?

HSA stands for a Health Savings Account. According to HealthCare.gov, a HSA is:

What is a Flexible Spending Account (FSA)?

Acording to HealthCare.gov, a Flexible Spending Account (also known as a flexible spending arrangement) is a special account you put money into that you use to pay for certain out-of-pocket health care costs. Here is more about FSA's from HealthCare.gov:

- FSAs are limited to $2,850 per year per employer. If you’re married, your spouse can put up to $2,850 in an FSA with their employer too.

-

You can use funds in your FSA to pay for certain medical and dental expenses for you, your spouse if you’re married, and your dependents.

- You can spend FSA funds to pay deductibles and copayments, but not for insurance premiums.

- You can spend FSA funds on prescription medications, as well as over-the-counter medicines with a doctor's prescription. Reimbursements for insulin are allowed without a prescription.

- FSAs may also be used to cover costs of medical equipment like crutches, supplies like bandages, and diagnostic devices like blood sugar test kits.

Will my company cover the cost of a standing desk?

If your insurance company does not cover the cost of your standing desk, your employer might. If your company has a wellness program, there is a likelihood they will be open to the idea of covering the cost of your standing desk.

The trend toward using standing desks at corporations is growing. Of the companies that have increased benefits offerings, 44% of them increased wellness benefits in 2018 alone.

The use of standing desks in wellness programs exploded from 20% to 53% from 2014 to 2018, as shown in the chart below from Society of Human Resource Management.

Final Thoughts:

As we have discussed in this article, not all insurers will reimburse you for the cost of a standing desk. First, call your insurance provider up to see if they do. If they do, you will most likely need to fill out a letter of medical necessity (LMN). You may be able to find your insurers LMN through a simple Google search.

NOTE: You will likely need your doctor to confirm the medical condition that you have that necessitates the need for a standing desk.

The other alternative is to ask your human resources department or head of wellness if they reimburse for standing desks. The trend toward use of standing desks is firmly intact so you may have good luck there.

Employers know the health and performance benefits of using a standing desk so they may be much more receptive to the idea. Best of luck and if you need help finding the perfect standing desk for you, check out our Desk Finder tool!